Any experienced backpacker knows that “packing light” is a relative term. What counts as a light pack for a Saturday morning day hike would be dangerously insufficient for a week-long trek through the Uintas.

The same logic applies to your financial “survival kit” your emergency fund.

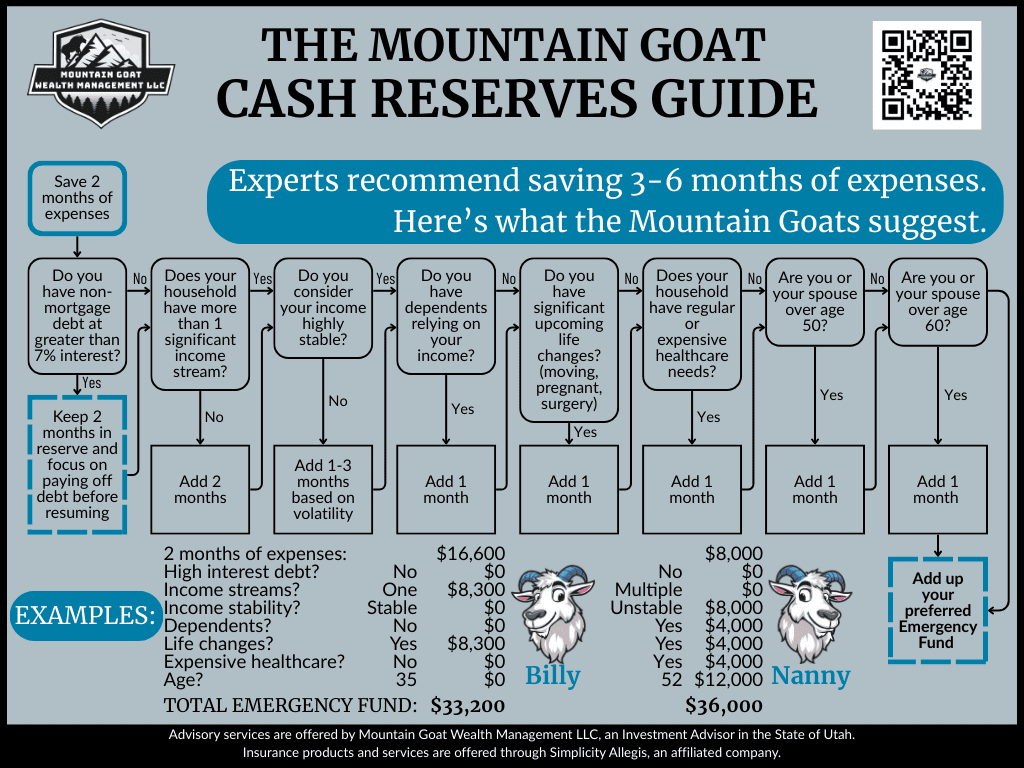

Common wisdom often throws out a blanket rule: “Save 3 to 6 months of expenses”. But just as you wouldn’t pack snowshoes for a desert hike, you shouldn’t rely on generic advice for your specific financial journey. At Mountain Goat Wealth Management, we believe your cash reserves should match the terrain you are navigating.

Here is how to calculate exactly how much “ration” you need in your pack.

1. The Base Weight: Start with 2 Months

Every journey starts with the essentials. We recommend everyone begin by saving 2 months of expenses. This is your baseline survival gear—enough to handle a sudden storm without weighing you down.

2. The “Heavy Pack” Check: High-Interest Debt

Before you add more weight to your reserves, check if you are already carrying a heavy load. Do you have non-mortgage debt with an interest rate greater than 7%?

If the answer is Yes: Stop here. Keep your reserves at 2 months and focus your energy on aggressively paying off that debt. High-interest debt is like hiking with rocks in your backpack; it drains your energy and slows your ascent. Lighten your load before you worry about stockpiling more supplies.

3. Assessing the Terrain: When to Pack More

If you don’t have high-interest debt, it is time to look at the trail ahead. Depending on the difficulty of your route, you may need to add to your base 2-month reserve. Ask yourself these questions:

Are you hiking on one “leg”? Does your household rely on a single significant income stream? If that one stream dries up, you are stuck on the mountain. If you do NOT have multiple income streams, add 2 months to your reserve.

Is the weather unpredictable? Do you consider your income highly stable? If you work on commission, are self-employed, or work in a volatile industry, perhaps you can’t predict the weather. If your income is NOT stable, add 1–3 months of reserves, depending on how volatile it is.

Are you guiding others? Do you have dependents relying on your income? When you are responsible for others on the trail, you need extra supplies. Add 1 month of reserves if this is you.

Is there a steep climb ahead? Do you have significant upcoming life changes, such as moving, a new baby, or planned surgery? Consider adding 1 month to cover the extra exertion.

How is your physical condition? Does your household have regular or expensive healthcare needs? You wouldn’t hike without a robust first-aid kit if you had a known condition. If yes, add 1 month.

How close is the summit? As you approach the summit of retirement, risk management becomes more critical. You have less time to recover from a fall. If you or your spouse are over age 50? Add 1 month. Over age 60? Add another 1 month.

Calculating Your Loadout

Your emergency fund isn’t just a random number; it’s a calculated decision based on your life’s landscape.

Scenario A: You might be a young professional with stable income but high student loans (high interest). You stick to the 2-month base to attack the debt.

Scenario B: You might be a couple in your 50s with one income source and kids in college. Your calculation might look like: Base (2 months) + Single Income (2 months) + Dependents (1 month) + Age 50 (1 month) = 6 months of reserves.

Don’t carry unnecessary weight, but don’t get caught in a storm unprepared.