For many, the word “budget” carries a restrictive connotation, evoking images of spreadsheets and sacrifice. However, in the realm of wealth management, a budget is not a constraint; it is a strategic tool that provides the clarity necessary to align your daily spending with your long-term financial aspirations. Improving your budget is less about “cutting back” and more about optimizing your cash flow to ensure that every dollar you earn is working toward your specific goals—whether that is early retirement, funding a child’s education, or building a legacy of charitable giving. By moving from passive observation to active management, you transform your budget from a record of the past into a roadmap for your future.

To refine your financial framework, consider these four essential strategies for budget optimization.

1. Conduct a Deep-Dive Cash Flow Analysis

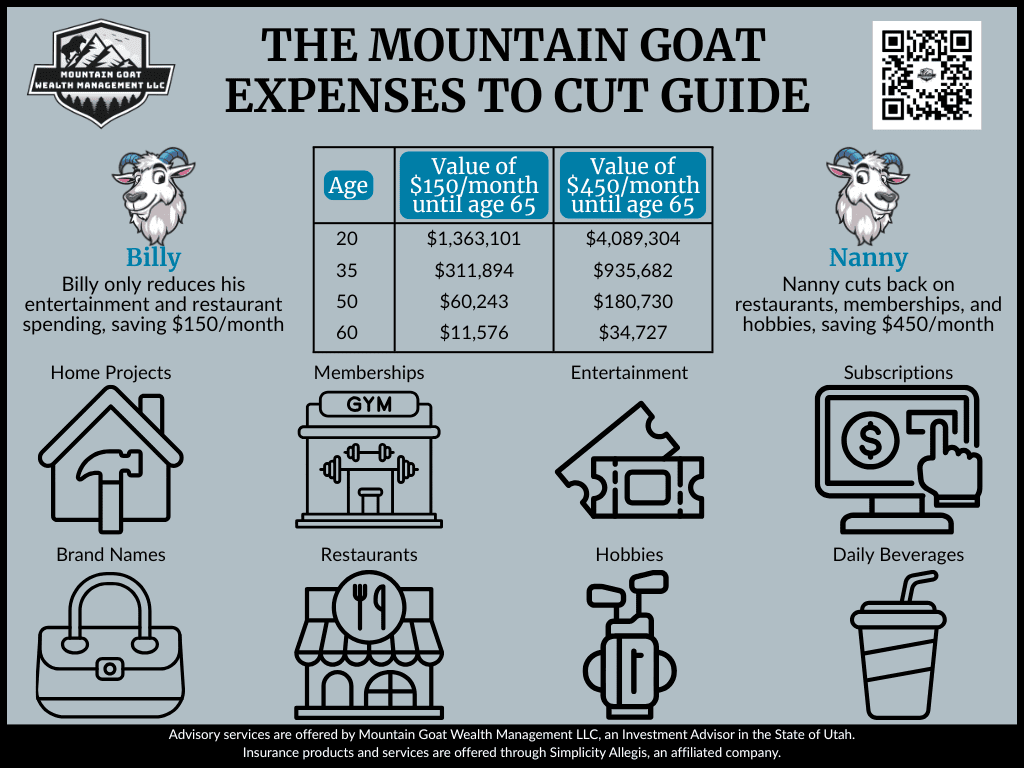

You cannot improve what you do not measure. The first step in refining a budget is a comprehensive audit of your “inflow” versus “outflow” over the last 90 days. Most individuals are surprised by the cumulative cost of “phantom expenses” such as recurring subscriptions you no longer use, convenience fees, and small daily purchases that aggregate into significant monthly sums.

To gain true clarity, categorize your spending into Fixed Expenses (mortgage, insurance, utilities) and Variable Expenses (dining out, travel, entertainment). This distinction is vital because it identifies your “levers.” While fixed expenses are harder to change in the short term, variable expenses provide immediate opportunities for optimization. Use this data to calculate your Savings Rate—the percentage of your gross income that remains after all expenses are paid. For a high-functioning budget, the goal is often to increase this rate systematically through incremental adjustments rather than drastic, unsustainable shifts.

2. Implement a Goal-Based Budgeting Framework

A common mistake in budgeting is focusing on the “limit” rather than the “purpose.” To improve your budget’s effectiveness, adopt a goal-based approach such as the 50/30/20 Rule or Zero-Based Budgeting.

- The 50/30/20 Rule: Allocates 50% of income to “Needs,” 30% to “Wants,” and 20% to “Savings and Debt Repayment.” This provides a simple macro-view of your financial health.

- Zero-Based Budgeting: This method involves assigning every single dollar a “job” until your income minus your expenses equals zero.

By tying your budget to specific objectives—such as “Travel Fund” or “Maxing out 401(k)”you create a psychological incentive to stick to your plan. When you view a potential purchase not as a standalone cost, but as a trade-off against a future goal, your spending habits naturally become more disciplined and intentional.

3. Automate the “Pay Yourself First” Principle

The most significant improvement you can make to any budget is removing the element of human willpower. Behavioral finance shows that we are much more likely to save when the decision is made for us. “Paying yourself first” means treating your savings and investment contributions as a non-negotiable “bill” that must be paid at the start of the month.

Work with your RIA to set up automated transfers from your checking account to your brokerage, IRA, or emergency fund accounts immediately following your payday. By automating these contributions, you effectively lower your “disposable” income to a level that reflects your actual spending capacity after your future is secured. This creates a “forced scarcity” that naturally keeps your lifestyle inflation in check without the need for constant daily monitoring of your bank balance.

4. Review, Adjust, and Account for Seasonality

A budget is a living document, not a static monument. One of the primary reasons budgets fail is a lack of flexibility. Life is rarely consistent; some months involve higher utility bills, while others include holiday gifts, annual insurance premiums, or property taxes. To improve your budget, you must account for this seasonality by creating “sinking funds”small monthly set-asides for these predictable but non-monthly expenses.

Furthermore, schedule a “Monthly Financial Date” with yourself or your spouse to review the previous month’s performance. Did you overspend in a certain category? Was there a windfall you didn’t account for? Use these reviews to adjust your targets for the following month. This iterative process ensures that your budget remains a relevant and helpful tool rather than a source of frustration. When your budget adapts to your life, you are much more likely to remain committed to it over the long haul.