In the modern financial landscape, your credit score is far more than just a number—it is a digital “reputation” that influences everything from the interest rate on your mortgage to the premiums you pay for auto insurance and even your eligibility for certain high-level employment opportunities.

As we navigate 2026, the mechanics of credit scoring have evolved significantly. Lenders have shifted away from simple “snapshots” of your debt and toward a more holistic view of your financial behavior, known as trended data. This means that your score is no longer just a reflection of what you owe today, but a predictive analysis of how you manage money over time.

Understanding where you stand in this new environment is the first step toward optimizing your financial leverage and ensuring that your credit acts as a bridge to your goals rather than a barrier.

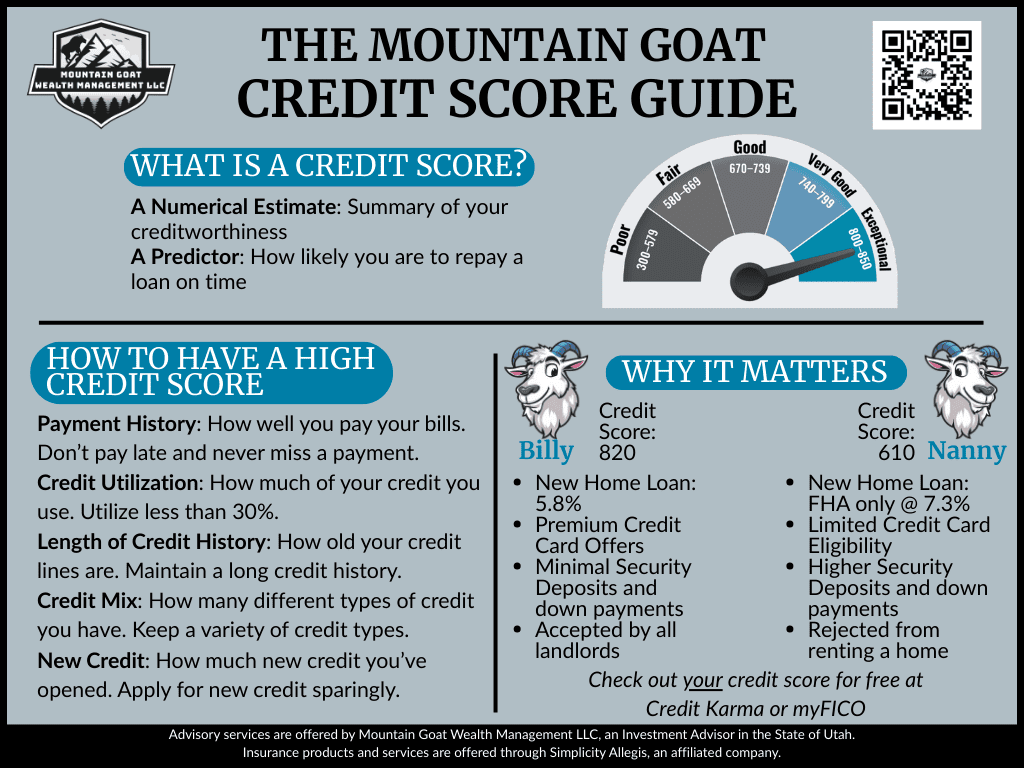

What Defines a “Good” Credit Score in 2026?

While there are dozens of different scoring models, the two most prominent are FICO and Vantage Score. For a standard FICO Score, which remains the benchmark for 90% of top lenders, the ranges are generally categorized as follows:

- Exceptional: 800–850

- Very Good: 740–799

- Good: 670–739

- Fair: 580–669

- Poor: 300–579

In 2026, a “good” score—specifically falling in the 670 to 739 range—typically qualifies you for most standard loan products. However, to access the “prime” interest rates that can save you tens of thousands of dollars over the life of a mortgage, you generally need to aim for a “Very Good” score of 740 or higher.

It is also important to note that as of late 2025 and early 2026, the mortgage industry has increasingly adopted Vantage Score 4.0 and FICO 10T. These newer models are more inclusive, often rewarding consumers who consistently pay down their balances month-over-month rather than those who simply make the minimum payment while carrying a large revolving debt.

The Architecture of Your Score: Key Factors

To improve your score, you must understand the “weights” that determine it. While the exact formulas are proprietary, they generally break down into five core categories:

- Payment History (35%): This is the single most influential factor. A single payment that is 30 days late can drop a high score by 100 points or more. In 2026, consistent on-time payments are viewed through the lens of longevity; the longer your streak of on-time payments, the more “resilient” your score becomes.

- Credit Utilization (30%): This represents the amount of credit you are using compared to your total limits. For example, if you have a $10,000 limit and a $3,000 balance, your utilization is 30%. For maximum score benefit, experts now recommend keeping this under 10%, though staying under 30% is the standard rule of thumb.

- Length of Credit History (15%): This considers the age of your oldest account, the age of your newest account, and the average age of all your accounts. Time is a powerful ally here; maintaining your oldest accounts, even if you rarely use them, provides the “depth” that lenders look for.

- Credit Mix (10%): Lenders like to see that you can manage different types of credit, such as “revolving” (credit cards) and “installment” (auto loans, mortgages, or personal loans).

- New Credit (10%): Opening multiple accounts in a short window or having too many “hard inquiries” can signal financial distress to a lender, causing a temporary dip in your score.

4 Strategic Steps to Boost Your Score

Improving your credit is a marathon, not a sprint, but there are several high-impact actions you can take to see results in a relatively short timeframe.

- Audit Your Reports for the “2026 Shift”: With the rise of automated reporting, errors have become more frequent. You are entitled to free weekly reports from the three major bureaus (Equifax, Experian, and TransUnion) via AnnualCreditReport.com. Look for incorrectly reported late payments or “zombie” debts that should have fallen off after seven years.

- Leverage Alternative Data: One of the most positive changes in 2026 is the ability to include non-traditional payments in your credit file. Tools like Experian Boost or programs that report your rent and utility payments can provide an immediate lift, especially for those with “thin” credit files.

- Master the “Trended Data” Game: Since newer models look at your balances over the last 24 months, focus on consistent de-leveraging. Instead of a one-time large payment to clear a card, try to show a steady downward trend in your total debt. This signals to the algorithm that you are a “transactor” (someone who uses credit and pays it off) rather than a “revolver” (someone who carries debt).

- Strategically Increase Limits: If you cannot immediately pay down a balance, call your credit card issuer and request a limit increase. If approved, this immediately lowers your utilization ratio—as long as you do not increase your spending to match the new limit.

By treating your credit score as a dynamic asset rather than a static grade, you can position yourself to take full advantage of the financial opportunities that 2026 has to offer.