In the modern professional landscape, understanding the specific retirement vehicle offered by your employer is a cornerstone of effective long-term financial planning. While all retirement plans share the ultimate goal of providing financial security in later years, the rules governing contributions, withdrawals, and employer matches vary significantly depending on whether you work for a private corporation, a non-profit, or a government entity. In 2026, as tax laws and contribution limits continue to evolve, knowing the nuances of your specific plan—be it a 401(k), 403(b), or a traditional Pension—can make a substantial difference in the size of your final nest egg. By strategically utilizing these employer-sponsored accounts, you can take advantage of tax-deferred growth and potential employer matching to accelerate your progress toward your financial “summit”.

The “Core Four”: 401(k), 403(b), TSP, and 457 Plans

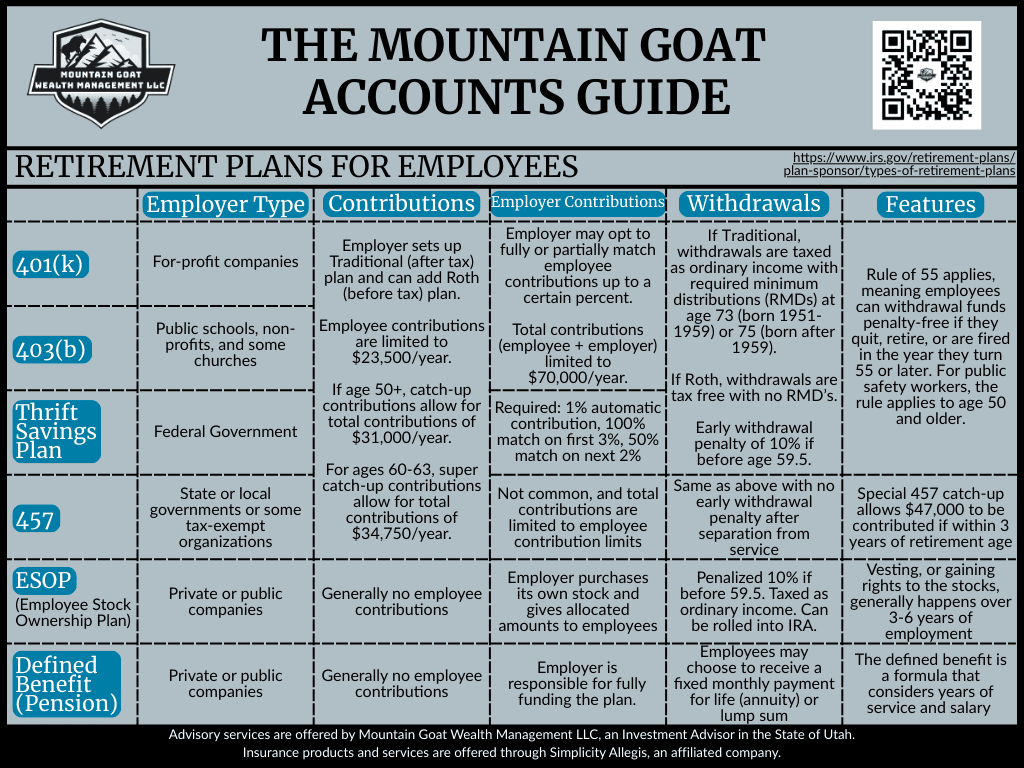

Most employees in 2026 are covered by one of four primary defined contribution plans, which are categorized by the type of employer that offers them:

- 401(k) Plans: The standard for for-profit companies. Employers set up these plans (often including both Traditional and Roth options) and may opt to fully or partially match employee contributions up to a certain percentage.

- 403(b) Plans: Specifically for employees of public schools, non-profits, and some churches. Like the 401(k), total contributions (employee + employer) are limited to $70,000 per year in 2026.

- Thrift Savings Plan (TSP): The retirement vehicle for the Federal Government. It features a highly structured matching system: a 1% automatic contribution from the employer, a 100% match on the first 3% of employee contributions, and a 50% match on the next 2%.

- 457 Plans: Offered by state or local governments and some tax-exempt organizations. These plans are unique because they typically have no early withdrawal penalty after you separate from service, regardless of your age.

For 401(k), 403(b), and TSP accounts, individual employee contributions are limited to $23,500 per year in 2026. However, those aged 50 and older can make “catch-up” contributions for a total of $31,000, while those aged 60–63 have a “super catch-up” limit of $34,750.

Ownership and Guarantees: ESOPs and Pensions

Beyond the standard contribution plans, some employers offer unique structures that provide either ownership stakes or guaranteed income:

- ESOP (Employee Stock Ownership Plan): In these plans, the employer purchases its own stock and allocates shares to employees, generally with no employee contribution required. Employees gain legal rights to these stocks through “vesting,” which typically occurs over 3–6 years of employment.

- Defined Benefit (Pension): These are traditional plans where the employer is responsible for fully funding the plan. Upon retirement, the employee receives a fixed monthly payment for life (an annuity) or a lump sum, based on a formula that considers their years of service and salary history.

Essential Rules for 2026 Withdrawals

Understanding when and how you can access your funds is critical to avoiding unnecessary penalties. Most plans incur a 10% penalty if funds are withdrawn before age 59.5, though exceptions like the “Rule of 55” allow employees who quit or are fired in the year they turn 55 (or 50 for public safety workers) to withdraw funds penalty-free.

Taxation depends on the “flavor” of your plan: withdrawals from Traditional plans are taxed as ordinary income, while Roth withdrawals are tax-free with no Required Minimum Distributions (RMDs). For those with Traditional accounts, RMDs must begin at age 73 (for those born 1951–1959) or 75 (for those born after 1959). By aligning your contribution strategy with these 2026 rules, you can maximize your employer’s “free money” while maintaining the flexibility needed for a successful retirement transition.