While knowing your target is vital, choosing where to house your savings is equally important. In 2026, the two most common types of IRAs offer distinct tax advantages.

1. Traditional IRA: Tax Benefits Today

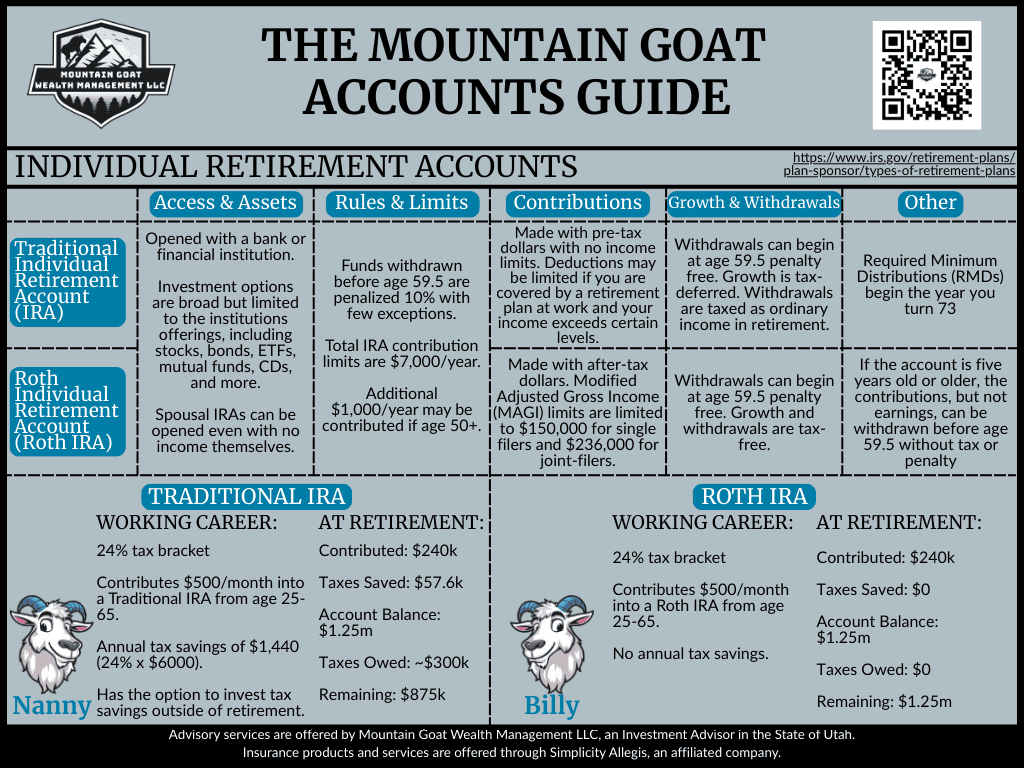

A Traditional IRA is funded with pre-tax dollars, meaning your contributions may be tax-deductible in the year they are made.

- Growth: Your investments grow tax-deferred; you don’t pay taxes on earnings until you withdraw the money.

- Withdrawals: Distributions are taxed as ordinary income. You must begin taking Required Minimum Distributions (RMDs) the year you turn 73.

- Best For: Those who expect to be in a lower tax bracket during retirement than they are today.

2. Roth IRA: Tax-Free Income Tomorrow

A Roth IRA is funded with after-tax dollars, so there is no immediate tax break.

- Growth: Your money grows tax-free.

- Withdrawals: Qualified distributions (after age 59½ and a 5-year holding period) are completely tax-free. Crucially, Roth IRAs have no RMDs during your lifetime.

- Best For: Younger investors or those who expect to be in a higher tax bracket in the future.

3. Specialty IRAs: For Small Business and Spouses

Beyond the “Big Two,” several other options exist for specific situations:

- SEP and SIMPLE IRAs: Designed for self-employed individuals and small business owners, these allow for much higher contribution limits than traditional IRAs.

- Spousal IRA: This allows a non-working spouse to contribute to their own IRA based on the working spouse’s earned income.

2026 Limits and Rules to Remember

For 2026, the annual contribution limit for both Traditional and Roth IRAs has increased to $7,500. If you are age 50 or older, you can contribute an additional $1,100 catch-up, totaling $8,600.

Keep in mind that while you can withdraw funds at any time, distributions before age 59½ typically incur a 10% penalty plus ordinary income taxes, unless an exception applies (such as a first-time home purchase or certain medical expenses). By carefully tracking your net worth and selecting the IRA type that aligns with your tax strategy, you ensure that your climb to financial independence is both efficient and secure.