Estate planning is often viewed through a narrow lens—a task reserved for the ultra-wealthy or something to be deferred until the “golden years.” However, in reality, estate planning is a vital component of a comprehensive financial strategy for anyone who wants to ensure their wishes are honored and their loved ones are protected. It is the process of arranging the management and transfer of your assets during your life and, more importantly, after your death. Beyond mere tax mitigation, a well-executed estate plan provides clarity during emotional times, prevents legal complications, and ensures that your legacy—both financial and personal—is preserved according to your specific values.

The process may seem daunting, but by breaking it down into systematic steps, you can move from uncertainty to peace of mind. Here are the five essential phases to building a robust estate plan.

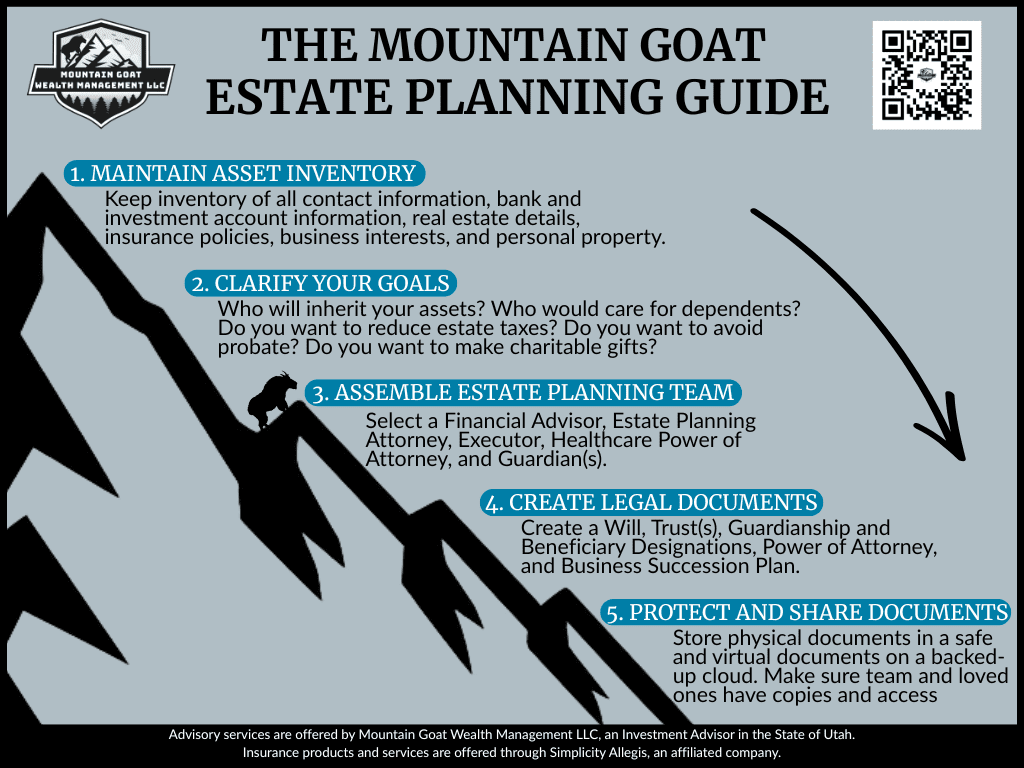

1. Maintain a Comprehensive Asset Inventory

The foundation of any estate plan is a clear understanding of what you actually own. You cannot effectively distribute assets if you haven’t accounted for them. Start by compiling a detailed inventory of your tangible assets, such as real estate, vehicles, jewelry, and collectibles. Equally important are your intangible assets: bank accounts, brokerage accounts, retirement plans (IRAs, 401(k)s), life insurance policies, and ownership interests in businesses.

In today’s world, you must also account for digital assets. This includes everything from cryptocurrency wallets to social media accounts and digital photo libraries. For each item, note the location of the physical asset or the login credentials for digital ones, as well as the estimated value and how the asset is currently titled (e.g., individual, joint tenancy, or held in a trust). This inventory serves as the roadmap for your legal documents and ensures that nothing is overlooked or lost in the probate process.

2. Clarify Your Goals and Objectives

Once you know what you have, you must decide what you want it to do. This stage is deeply personal and requires honest reflection. Ask yourself: Who do I want to inherit my assets? Do I want to provide for my spouse first, or pass wealth directly to children? If you have minor children, who would you trust to be their legal guardian?

Beyond simple distribution, consider your legacy goals. Perhaps you want to fund a grandchild’s education, support a specific charity, or ensure a family business continues to thrive under new leadership. This is also the time to consider “what if” scenarios regarding your own health. Clarifying your wishes regarding medical intervention and end-of-life care is just as much a part of estate planning as distributing money. By defining these goals early, you provide your advisors with the “why” behind the “how,” allowing them to tailor legal structures to your specific vision.

3. Assemble Your Estate Planning Team

Estate planning is not a DIY project. Because it involves complex intersections of tax law, state-specific statutes, and financial management, you need a team of professionals working in concert. Your core team should typically include:

- An Estate Planning Attorney: To draft the legal documents and ensure they comply with current laws.

- A Financial Advisor/RIA: To ensure your estate plan aligns with your broader investment strategy and long-term financial goals.

- A Tax Professional (CPA): To minimize the tax burden on your heirs and maximize the efficiency of asset transfers.

A collaborative approach is essential. For instance, your RIA can work with your attorney to ensure that your account beneficiaries are aligned with your Will or Trust, preventing a common mistake where outdated beneficiary designations override the instructions in a Will.

4. Create and Execute Legal Documents

With your goals set and your team in place, it is time to codify your wishes into legally binding documents. While every plan is unique, a standard “estate planning package” usually includes:

- Last Will and Testament: Outlines who receives your assets and names executors and guardians.

- Revocable Living Trust: Often used to avoid probate, provide privacy, and manage assets if you become incapacitated.

- Durable Power of Attorney: Designates someone to handle your financial affairs if you cannot.

- Healthcare Power of Attorney and Living Will: Appoints a healthcare proxy and specifies your preferences for medical treatment.

These documents are the engines that drive your plan. It is crucial to ensure they are signed, witnessed, and notarized according to your state’s specific legal requirements to ensure their validity when they are needed most.

5. Protect and Share Your Documents

A perfect estate plan is useless if no one can find it. Once your documents are executed, they must be stored in a secure yet accessible location. While a fireproof safe at home or a bank safety deposit box are common choices, ensure that your Executor or Successor Trustee knows exactly where the keys or codes are located.

Furthermore, “protecting” your plan also means “sharing” the intent behind it. While you don’t necessarily need to disclose every dollar amount, having a family meeting to discuss your general wishes can prevent future conflicts and litigation. Finally, remember that estate planning is not a one-time event. You should review and update your plan every three to five years, or after major life events such as marriage, divorce, the birth of a child, or significant changes in tax law. By keeping your plan current, you ensure that your legacy remains a gift to your loved ones, rather than a burden.