On any major expedition, managing your resources is just as critical as the climb itself. You wouldn’t drink all your water at the trailhead, nor would you wait until you’re dehydrated at the summit to take a sip. Social Security is much the same—it is a vital supply cache for your retirement journey but deploying it at the right elevation can make all the difference in how comfortably you finish the trek.

At Mountain Goat Wealth Management, we help you scout the terrain to determine exactly when you should tap into this resource.

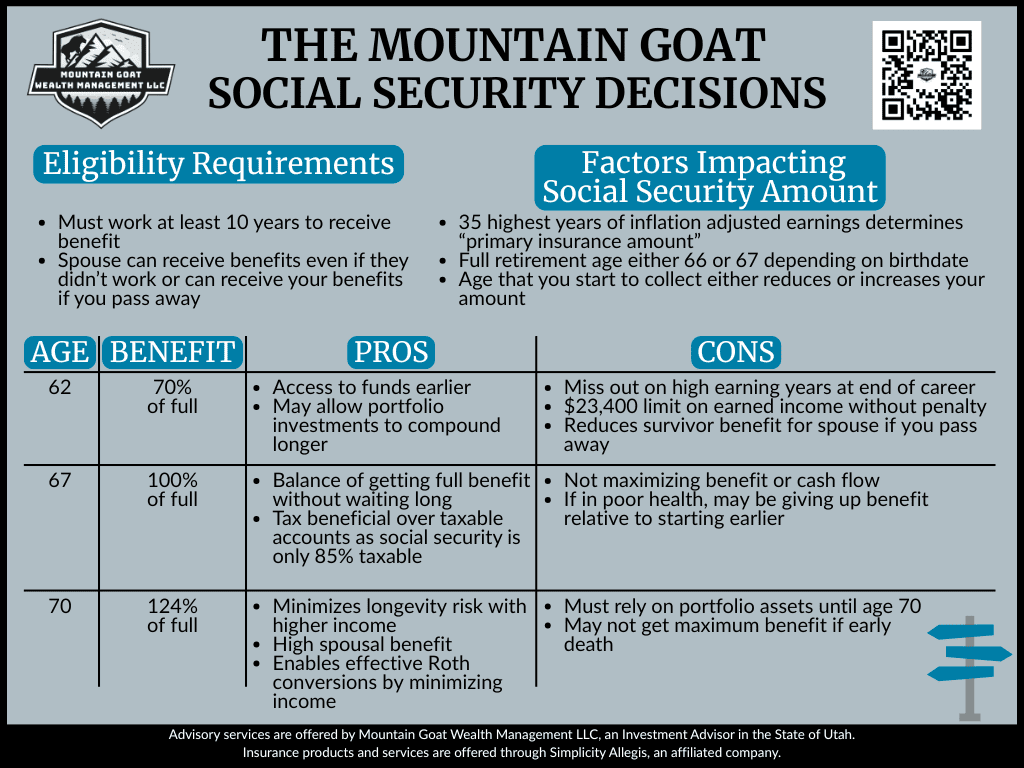

Earning Your Stripes: Eligibility

Before you can count on this supply drop, you have to earn your place on the mountain. According to the Social Security Administration, you generally must work at least 10 years to receive benefits.

However, the system also protects your climbing partner. A spouse can receive benefits even if they didn’t work the required 10 years, or they can receive your benefits as a survivor if you pass away. This “belay” system ensures that your team isn’t left stranded on the face of the mountain.

Mapping the Route: How It Is Calculated

Your benefit isn’t a random number; it is calculated based on the terrain you’ve already covered. The government looks at your 35 highest years of inflation-adjusted earnings to determine your “primary insurance amount”.

Your “Full Retirement Age” (the standard altitude for full benefits) is usually 66 or 67, depending on your birth year. But just like a climber can choose to push for the summit early or wait for better weather, you have options.

Choosing Your Path: Three Major Trailheads

The age you choose to start collecting benefits significantly alters your financial altitude.

1. The Early Start: Age 62 (70% of Full Benefit)

This is the earliest you can start the climb.

- The View: You get access to funds sooner, which preserves your other portfolio investments, allowing them to compound longer.

- The Risk: You only receive 70% of your full benefit. If you are still working, there is a strict limit on earned income ($23,400) before penalties kick in. Perhaps most importantly, taking it early permanently reduces the survivor benefit for your spouse if you pass away.

2. The Standard Route: Age 67 (100% of Full Benefit)

This is the balanced approach—the base camp of retirement planning.

- The View: You receive 100% of your benefit, striking a balance between getting paid and not waiting too long. It can also be tax-beneficial compared to drawing from taxable accounts, as Social Security is often only 85% taxable.

- The Risk: You aren’t maximizing the potential cash flow. If you are in poor health, waiting this long might mean giving up benefits relative to starting earlier.

3. The High Summit: Age 70 (124% of Full Benefit)

For those prepared to endure the wait, the view from here is spectacular.

- The View: You receive 124% of your full benefit. This minimizes “longevity risk” (running out of money if you live a long time) and secures a high spousal benefit. It also enables savvy moves like Roth conversions in your 60s by keeping your taxable income low.

- The Risk: You must rely entirely on your own portfolio assets until age 70. There is also the grim reality that if you pass away early, you may not get the maximum lifetime benefit.

Tales from the Trail: Real World Examples

The “Base Camp” Hikers Imagine a couple, John and Sarah. John has health concerns and wants to enjoy his early 60s while mobile. He chooses the Age 62 route. He accepts the 70% payout to fund travel now. However, he must be careful not to earn more than $23,400 working part-time, or he’ll face penalties.

The “High Altitude” Alpinist Elena is healthy, loves her job, and plans to live to 95. She waits until Age 70. By relying on her savings in her 60s, she performs Roth conversions to lower her future taxes. When she hits 70, she unlocks the massive 124% benefit, ensuring she has a heavy stream of income no matter how long her expedition lasts.

Your Next Step

There is no single “correct” trail, only the one that fits your expedition. Are you ready to chart your course?