In the backcountry, elevation is everything. It tells you how far you’ve come, how much terrain is left to conquer, and whether you are on track to reach the summit before sundown. In your financial life, “Net Worth” is your elevation.

Just as a mountain goat navigates rocky slopes with precision and confidence, you need a sure-footed metric to track your financial progress. But how do you calculate it, and more importantly, is your current elevation high enough for your age?

Let’s check your coordinates.

The Gear Check: What is Net Worth?

Before you start climbing, you must know what you’re carrying. Your net worth isn’t just your salary; it’s a snapshot of your entire financial backpack.

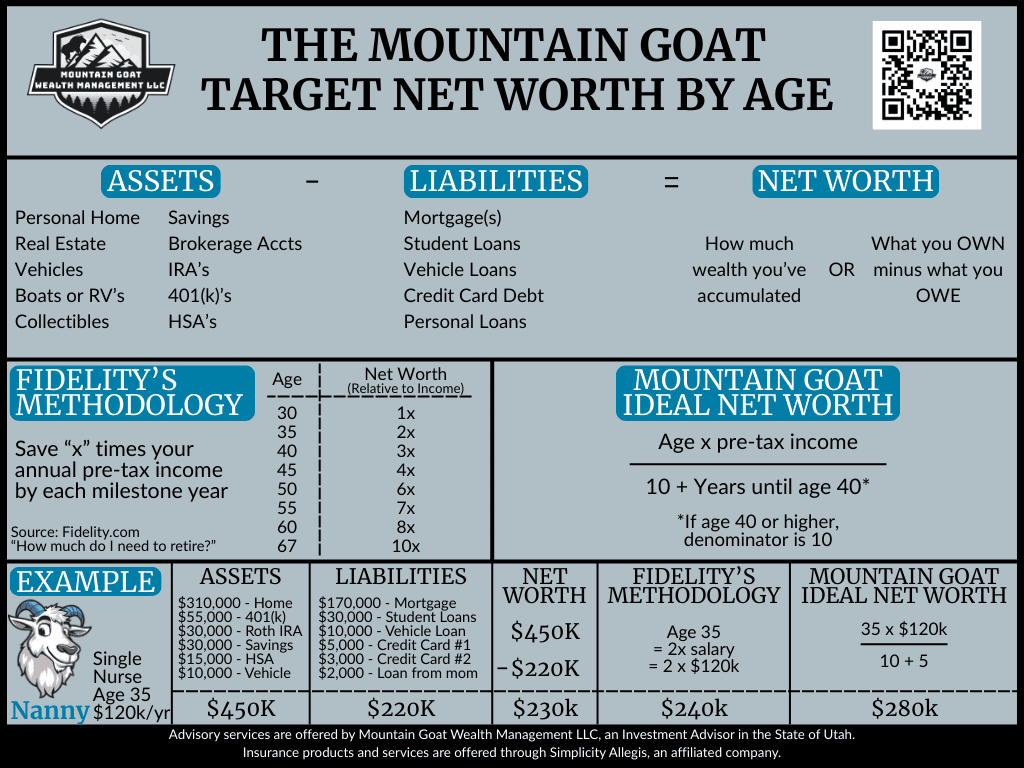

Net Worth = Assets – Liabilities

- Assets (What You Own): This is your gear, the positive value in your pack. It includes your home, real estate, vehicles, recreational toys (boats, RVs), collectibles, and all investment accounts (Savings, Brokerage, IRAs, 401(k)s, HSAs).

- Liabilities (What You Owe): This is the dead weight slowing you down. It includes mortgages, student loans, vehicle loans, credit card debt, and personal loans.

Subtract the weight of your liabilities from the value of your assets. The result is your financial altitude.

Trail Markers: Fidelity’s Methodology

Fidelity Investments has marked the trail with general milestones to help climbers see if they are keeping pace. Their methodology suggests saving a specific multiple of your annual pre-tax income by certain ages.

Think of these as signposts along the trail:

- Age 30: 1x your annual income

- Age 40: 3x your annual income

- Age 50: 6x your annual income

- Age 60: 8x your annual income

- Age 67: 10x your annual income

If you are earning $100,000 at age 40, Fidelity suggests you should have about $300,000 in saved wealth to be on track for a comfortable retirement.

The Summit Push: Mountain Goat Ideal Net Worth

While Fidelity provides excellent trail markers, at Mountain Goat Wealth Management, we like to look at the steeper, more aggressive routes. We use a formula that adjusts for your specific age, pushing you to build wealth like a “Prodigious Accumulator.”

The Formula:

(Age X Pre-Tax Income) / (10 + Years Until Age 40)

- If you are under 40: The denominator is 10 plus the number of years left until you turn 40.

- If you are 40 or older: The denominator locks in at 10.

This formula accounts for the fact that younger climbers have had less time for compound interest to work, while older climbers should have a stronger foothold.

Views from the Ridge: Real World Examples

Let’s look at two climbers on the mountain to see how the math plays out.

Example 1: The Young Climber

Meet a 35-year-old Single Nurse earning $120,000/year.

- Assets: $450k (Home, 401k, Roth IRA, Savings)

- Liabilities: $220k (Mortgage, Student Loans, Car Loan)

- Actual Net Worth: $230,000

How does she compare?

- Fidelity’s Benchmark (2x Salary): $240,000

- Mountain Goat Ideal:

- Step 1: Calculate numerator ($35 x $120,000 = $4,200,000)

- Step 2: Calculate denominator ($10 + 5 years to 40 = 15)

- Target: $4,200,000 / 15 = $ $280,000

She is currently at $230k. She is slightly below the ridge but well within striking distance of the summit path.

Example 2: The Seasoned Alpinist

Consider a 50-year-old Manager earning $150,000/year.

- Fidelity’s Benchmark (6x Salary): $900,000

- Mountain Goat Ideal:

- Since he is over 40, the denominator is 10.

- Calculation: (50 x 150,000) / 10

- Target: $750,000

In this case, the Mountain Goat formula is more forgiving than the general Fidelity benchmark, acknowledging that high earners may have started later or have different cash flow needs.

Keep Climbing

Whether you are in a valley looking up or standing on a peak, the most important step is the next one. Calculate your net worth today, check your bearings against these formulas, and keep moving upward. The view from the top is worth it.